“`html

Calculating Finance Payments

Understanding how to calculate finance payments is crucial for managing personal finances and making informed decisions about loans, mortgages, and leases. At its core, a finance payment calculation determines the periodic amount you’ll need to pay to cover both the principal (the original loan amount) and the interest accrued over the loan’s term.

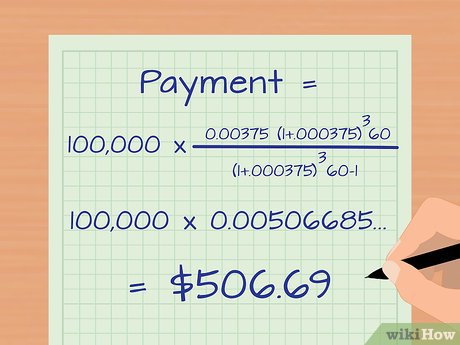

The most common formula used is for a fixed-rate amortizing loan, where payments are made regularly (e.g., monthly) and remain constant throughout the loan term. The formula looks like this:

M = P [ i(1 + i)^n ] / [ (1 + i)^n – 1]

Where:

- M = Monthly Payment

- P = Principal Loan Amount (the initial amount borrowed)

- i = Monthly Interest Rate (annual interest rate divided by 12)

- n = Number of Payments (loan term in months)

Let’s break down how to use this formula with an example. Suppose you borrow $20,000 (P) at an annual interest rate of 6% (6/100 = 0.06) for a term of 5 years (5 * 12 = 60 months). First, calculate the monthly interest rate: 0.06 / 12 = 0.005. Then, plug the values into the formula:

M = 20000 [ 0.005(1 + 0.005)^60 ] / [ (1 + 0.005)^60 – 1]

Solving this equation gives you a monthly payment of approximately $386.66.

While this formula provides a solid understanding of the calculation, it’s often easier to use online calculators or spreadsheet programs like Microsoft Excel or Google Sheets. These tools have built-in functions that simplify the process. In Excel or Google Sheets, you can use the PMT function. The syntax is: PMT(rate, nper, pv, [fv], [type]).

Using our example: =PMT(0.06/12, 60, 20000) would return the same monthly payment of approximately $386.66. (The result may be negative, indicating a payment outflow.)

When using these tools, remember to double-check the inputs. Ensure you’re using the correct interest rate (annual vs. monthly), loan amount, and loan term. Incorrect inputs will lead to inaccurate payment calculations.

Beyond simple loan calculations, understanding these principles allows you to analyze the total cost of a loan (total payments made, including interest), compare different loan offers, and make informed financial decisions. Always consider the impact of interest rates and loan terms on your monthly payments and overall financial burden.

“`

728×546 ways calculate loan payments wikihow from www.wikihow.com

728×546 ways calculate loan payments wikihow from www.wikihow.com  728×546 ways calculate mortgage payments wikihow from www.wikihow.com

728×546 ways calculate mortgage payments wikihow from www.wikihow.com  728×546 calculate mortgage payments examples wikihow from www.wikihow.com

728×546 calculate mortgage payments examples wikihow from www.wikihow.com  460×345 ways calculate interest payments wikihow life from www.wikihow.life

460×345 ways calculate interest payments wikihow life from www.wikihow.life  1200×1200 number payments calculator repayments calculator finance calcul from finance.icalculator.com

1200×1200 number payments calculator repayments calculator finance calcul from finance.icalculator.com  1125×298 answered calculate amount financed bartleby from www.bartleby.com

1125×298 answered calculate amount financed bartleby from www.bartleby.com  1200×675 calculate monthly payments loan wise loan from wiseloan.com

1200×675 calculate monthly payments loan wise loan from wiseloan.com  576×108 calculate payment from btacinc.com

576×108 calculate payment from btacinc.com  826×1024 finance calculators avenyou from www.avenyou.net.au

826×1024 finance calculators avenyou from www.avenyou.net.au  1280×720 calculate loan payments pmt function excel from www.theworldhour.com

1280×720 calculate loan payments pmt function excel from www.theworldhour.com  1216×832 loan calculator singapore calculate monthly payments quickly from kaizenaire.com

1216×832 loan calculator singapore calculate monthly payments quickly from kaizenaire.com  1600×1197 finance calculator ramneek singh dribbble from dribbble.com

1600×1197 finance calculator ramneek singh dribbble from dribbble.com  1000×667 calculate monthly loan payment minute cash mart singapore from cashmart.sg

1000×667 calculate monthly loan payment minute cash mart singapore from cashmart.sg  720×540 calculating payments powerpoint id from www.slideserve.com

720×540 calculating payments powerpoint id from www.slideserve.com  1600×1157 calculating payments stock photo image calculate risk from www.dreamstime.com

1600×1157 calculating payments stock photo image calculate risk from www.dreamstime.com  1020×672 finance calculators calculoidcom from www.calculoid.com

1020×672 finance calculators calculoidcom from www.calculoid.com  728×546 easy ways calculate annual payment loan from www.wikihow.com

728×546 easy ways calculate annual payment loan from www.wikihow.com  2000×1045 finance information from www.lowryjewellers.com

2000×1045 finance information from www.lowryjewellers.com